Portfolio maintenance in turbulent times

Since the outbreak of the Iran conflict, market losses have been limited, at least so far. But it might not take much in terms of adverse developments in the Middle East to wipe out any remaining positive year-to-date returns. Patience and defensiveness tend to point to cash, short-duration and inflation-linked assets as a viable tactical stance until the fog of war clears.

- Key macro themes – We await more material changes to economic and central bank forecasts

- Key market themes – Volatility driven by headlines but no obvious market ‘cheapness’

A spectrum of outcomes

Investors continue to face the risk that the Middle East conflict might (re)escalate further. Recent developments, however, have also suggested a ceasefire is possible, which would bring some relief to oil markets.

While markets have been disrupted significantly in recent weeks, drawdowns have largely stopped short of major corrections. Of the major equity markets, only the Korean KOSPI and the MSCI Emerging Markets indices have corrected by more than 10% from their recent highs.

There also remains a scenario in which markets must price in a tightening of monetary policy as central banks lean against higher short-term inflation becoming embedded in expectations.

However, the interest rate path is unclear, and arguably, markets have done quite a bit of tightening for central banks already. Since the conflict began bond yields have moved higher, while equity markets are materially lower.

Confidence in any scenario in the coming days and weeks is necessarily low. This provides a significant challenge to making investment decisions. The timing and characteristics of the optimal exit point are unknown.

Value hunting

Have markets moved enough to reveal value opportunities? An argument that markets are too negative on the interest rate outlook is valid, despite central bankers’ hawkish shift. But this is not 2022. Back then the US Federal Reserve started raising rates - a month after the Russia’s invasion of Ukraine - from a starting level of 0.5% and when consumer price inflation had already climbed to 8%. The situation was similar for the European Central Bank and the Bank of England.

Inflation is going to move higher. That is a given. But rates are higher than they were in 2022 - real rates are much higher - and the inflation tailwinds have been more favourable. In a de-escalation scenario, oil prices should ease and, although energy costs overall will remain elevated, the pass-through to consumer prices might be modest in terms of size and duration.

Given we are already observing higher forward rates, the question of whether central banks need to follow through is a valid one. If one believes they do not have to, then shorter maturity fixed income assets look attractive – US two-year Treasury yields are 3.93%; in Europe yield ranges from 2.68% in Germany to almost 3% in Italy; and in the UK the two-year gilt yield is 4.5%.

It is hard to make the case that rates will rise more than is currently priced in. Add on a 15 to 20 basis point widening in credit spreads since 27 February, and short-duration investment grade credit does look attractive - high yield potentially even more.

Investors may also want to look at floating rate instruments in this environment. In addition, higher consumer price indices will boost returns from short-duration inflation-linked bond strategies in the coming months.

Little is cheap

The broader view is that a limited number of assets have materially cheapened, but they tend to be those that responded to concerns around artificial intelligence disruption or private credit concerns before Iran rather than the conflict itself.

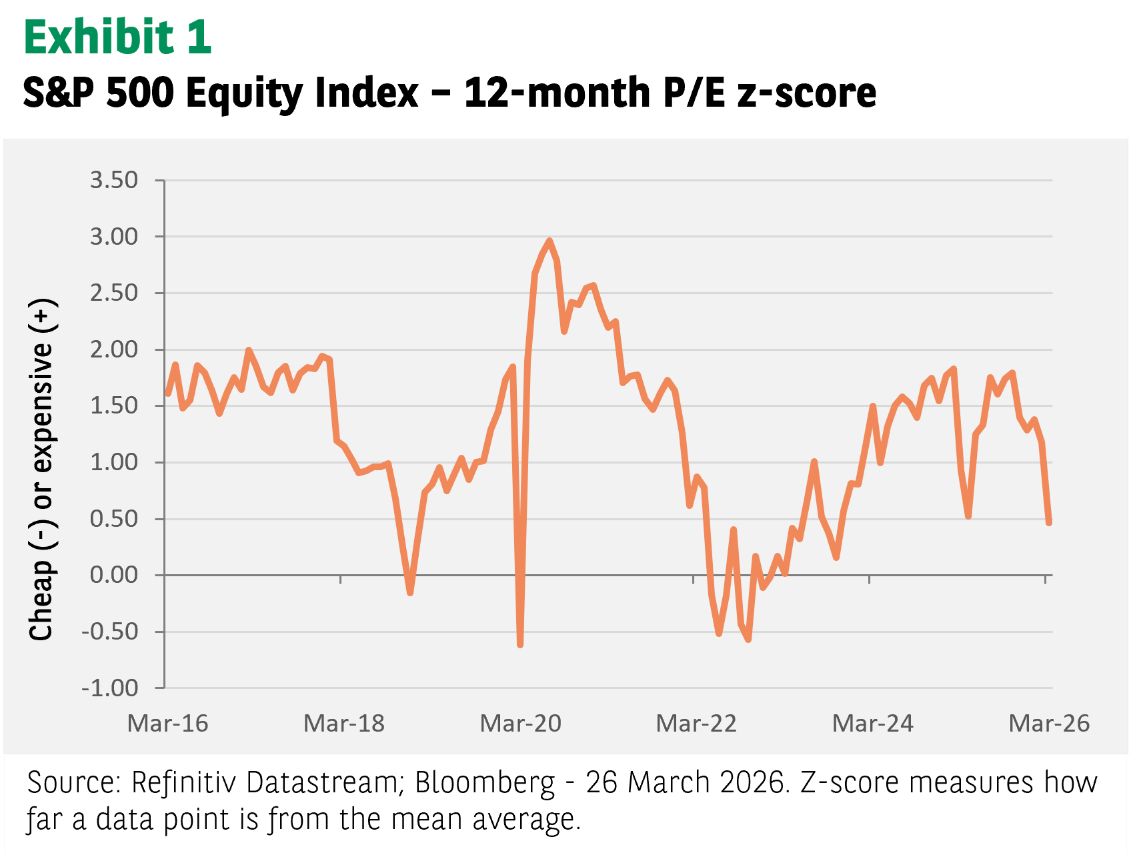

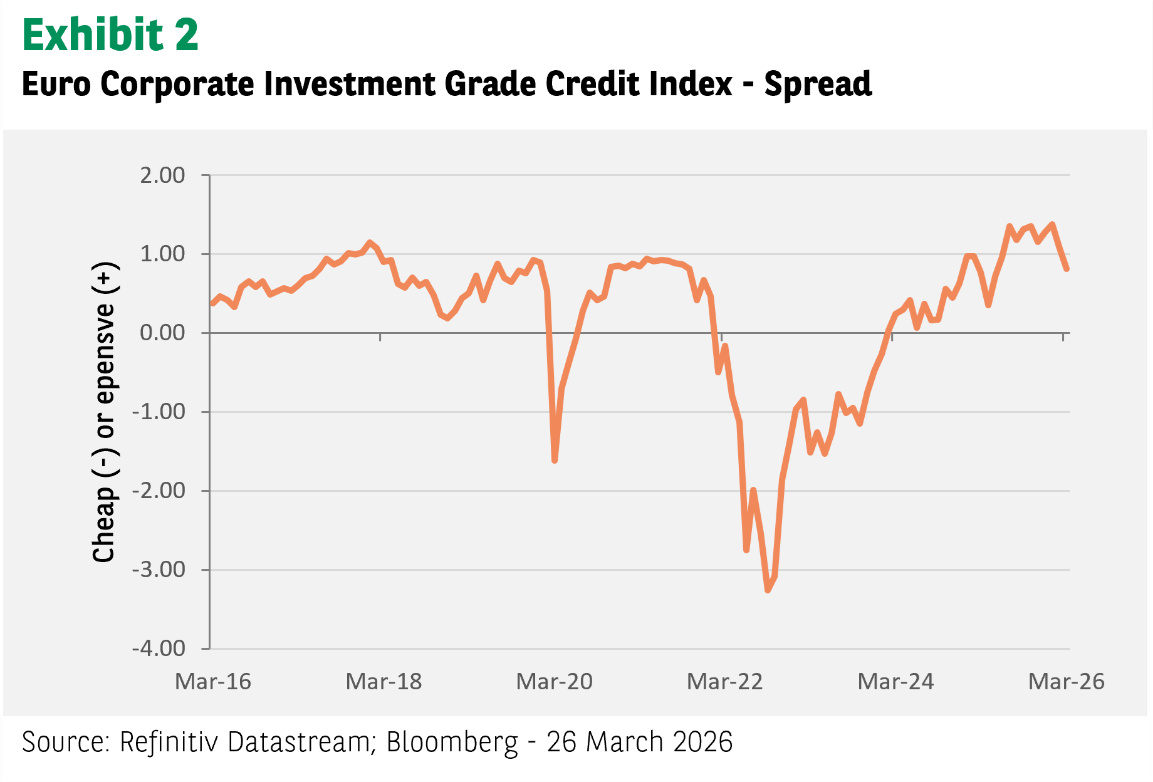

I looked at where 12-month price-to-earnings ratios for equities, and option-adjusted spreads for credit, stand after more than three weeks of conflict relative to their averages of the last three years.

Asset classes which have cheapened the most since the start of the year (relative to their three-year average) include the Nasdaq and S&P 500 indices – notably the Information Technology and Financials sectors of the latter index as well as the global MSCI Emerging Markets equity index. European and US high yield indices are also cheaper because of higher spreads.

Taking a longer-term view, however, it is difficult to see any real market ‘cheapness’. The Nasdaq, US small caps, and global emerging markets are trading on P/E ratios just below their 10-year averages. Other equity markets, including the S&P 500, remain at a premium to longer-term valuation metrics.

On the metric used here, Europe, the UK and Japan were much cheaper in 2022. In credit, spreads are still well below their 10-year average levels, except for the small technology and electronics sector of the US high yield market. So, while most markets are lower, in fixed income the real shift in value has been the rise in underlying rates curves. The real (inflation adjusted) US 10-year Treasury rate is back above 2.0% for the first time since mid-2025.

Risk premiums have risen but not by enough to compensate investors for the still possible very adverse scenario in the Middle East.

Defence is the best form of attack

It is a challenging time to manage portfolios. There is an incentive to hold more cash and cash-like assets, and those that offer inflation protection. Economists are starting to revise down growth forecasts but material revisions to equity earnings forecasts have not happened yet.

The risk is that, as we get more corporate guidance around the first quarter earnings season, growth forecasts will be lowered. That is the risk for equities, while the ongoing flow of negative headlines around private credit might, at some point, infect the public credit markets (they should not from a fundamental point of view, but sentiment is often dislodged from fundamentals).

A scenario of higher equity volatility (the VIX volatility index is only at 27; it reached 50 around ‘Liberation Day’ last year), lower equity prices and wider credit spreads cannot be ruled out, conditional on how things evolve in the Gulf. Having cash-like liquidity can be an advantage in such circumstances.

Being patient is a virtue and a necessity for longer-term investors. Gradually locking in higher risk premiums without betting on a rapid return of market prices to pre-conflict levels seems a sensible approach.

Headline risk remains high, shifts in sentiment are binary, depending on fluctuations in the price of Brent crude. A cessation of hostilities is the very minimum that investors should require before there is more confidence in committing capital to higher return assets.

Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, BNP Paribas AM, as of 26 March 2026, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.