Take Two: Central banks leave interest rates unchanged, and oil prices rise

What do you need to know?

The US Federal Reserve left interest rates on hold at 3.50%-3.75% but its members were divided over the path of future policy. One policymaker voted for a 25-basis-point cut while three of the 12 committee members agreed with the decision to maintain the target range, but “did not support the inclusion of an easing bias in the statement at this time”. The last time four members dissented was in 1992. Separately, an official advance estimate showed the US economy grew at an annual rate of 2% in the first quarter of 2026, up from 0.5% in Q4 2025.

Around the world

The European Central Bank left interest rates on hold, keeping its main deposit rate at 2% and warning that “upside risks to inflation and the downside risks to growth have intensified” amid the Middle East conflict. Eurozone inflation rose to 3% in April from 2.6% in March, a flash estimate showed, while core inflation – excluding energy, food, alcohol and tobacco – eased slightly to 2.2% from 2.3%. Meanwhile the bloc’s economy expanded by 0.1% in Q1, a slight slowdown from Q4’s 0.2%. Elsewhere, both the Bank of England and the Bank of Japan kept interest rates unchanged.

Figure in focus: 24%

Energy prices are forecast to rise 24% this year on the back of the Middle East conflict, their highest level since Russia’s invasion of Ukraine in 2022, according to a new report from the World Bank. Overall, commodity prices are expected to rise 16% in 2026, driven by rising energy costs and record prices for several key metals. Meanwhile, the price of Brent crude oil rose to over $126 a barrel - its highest level since 2022 - last week before later easing back, after reports that peace talks between the US and Iran had stalled. Elsewhere, the MSCI Emerging Markets index rose to a record high, bolstered by gains in semiconductor stocks.

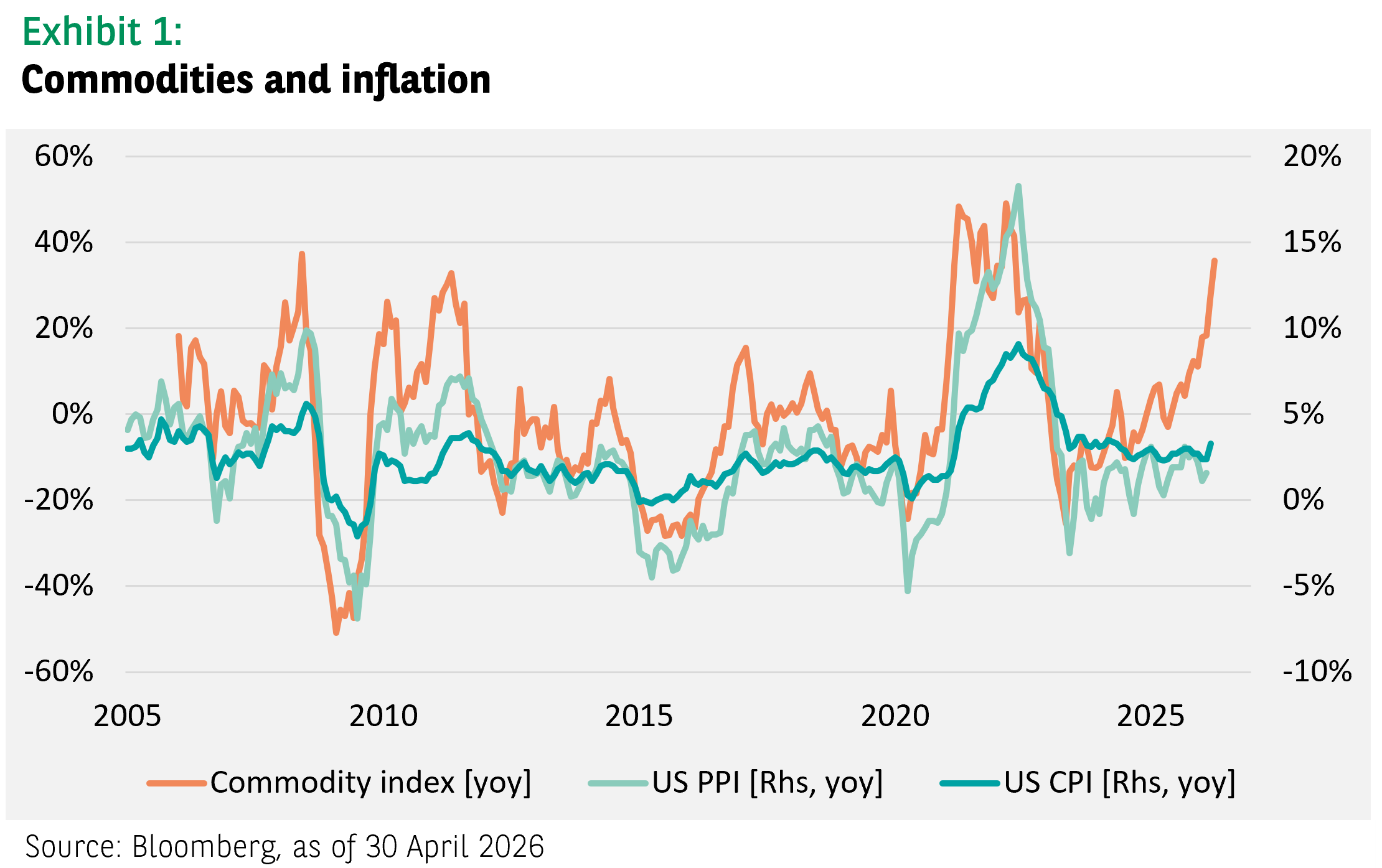

Chart of the week

The Middle East conflict is pushing up the price of commodities, in particular those which are energy related. The year-on-year change in the Bloomberg Commodity Index is not too distant from 40%, a level that might be associated with an accelerating producer and consumer inflation rate. While central bankers have tended to look through such temporary commodity price shocks, there is a risk of a prolonged increase in prices, which might hurt consumer spending. Shorter-duration government bonds, as well as limited exposure to long-dated government bonds, could potentially help mitigate the risk if interest rates were to rise sharply.

Words of wisdom

Coal fuel cells: Researchers in China have developed a new method of generating electricity from coal that does not use combustion and cuts carbon emissions. Zero-carbon-emission direct coal fuel cells use a process where coal is turned into a powder and placed inside a fuel cell to create a chemical reaction which generates electricity. The carbon dioxide produced by the reaction is captured and then transformed into other compounds, potentially enabling a cleaner use of fossil fuels. Researchers say the process could also be used underground, meaning coal would potentially not need to be mined and transported to the surface.

What’s coming up?

On Tuesday the Reserve Bank of Australia convenes to set interest rates while the US reports its final composite Purchasing Managers’ Index for April. The Eurozone, UK and China follow with their composite PMI data on Wednesday. Thursday sees the Bank of Japan publish the minutes of its previous monetary policy meeting while the Eurozone reports retail sales figures. Japan follows on Friday with its final composite PMI data and the US reports jobs numbers.

Read more insights at the Investment Institute

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.