Emerging Markets Outlook – living on the (dollar) edge

Key points

- Emerging markets (EM) are on a structurally sounder footing amid tighter global financial conditions. Access to international capital markets may remain difficult for some frontier markets

- We expect growth recovery in Central Europe and Asia, but diverging trends within Latin America

- The monetary easing cycle will likely be shallow, guided by the Fed’s stance and domestic disinflation. Fiscal consolidation could be limited by a heavy electoral year across EM regions in 2024

This is not the 1990s

The expected “high for long” scenario of US monetary policy is reminiscent of the 1990s which saw a series of major crises in emerging markets (EM): the 1994 Mexican ‘Tequila’ crisis, the 1997 Asian financial crisis and the 1998 Russian crisis. For sure, high real US yields and a strong dollar will continue to exert pressures on many countries, particularly those in already precarious financial positions which rely extensively on hard currency borrowing. Easy global financial conditions post the global final crisis allowed many frontier market (FM) economies to raise unprecedented amounts of capital on international bond markets. Sovereign issuance remained particularly depressed for most FMs for a second year in a row in 2023, while some countries lost market access altogether. Several countries are in advanced debt restructuring negotiations, and multilateral funding has increasingly stepped in to help cover governments’ financing needs. Fragile situations needing close monitoring remain in Egypt or Kenya, to name some.

Beyond this specific market segment, EMs are undeniably structurally and institutionally better equipped to face external headwinds than they were during the 1990s. Local debt markets have developed significantly, decreasing their reliance on external financing; exchange rates have been allowed to float, reducing pressure builds; institutional credibility is higher with central banks better able to anchor inflation expectations and to ensure financial stability thanks to foreign exchange reserves management while banking systems are also better capitalised. There are of course exceptions; for example Argentina or Turkey, but a general structurally-sounder footing should limit the risk of a systemic crisis. Moreover, portfolio outflows from EM debt markets for the past two years signal light foreign investors’ positioning.

Growth divergence between and within regions

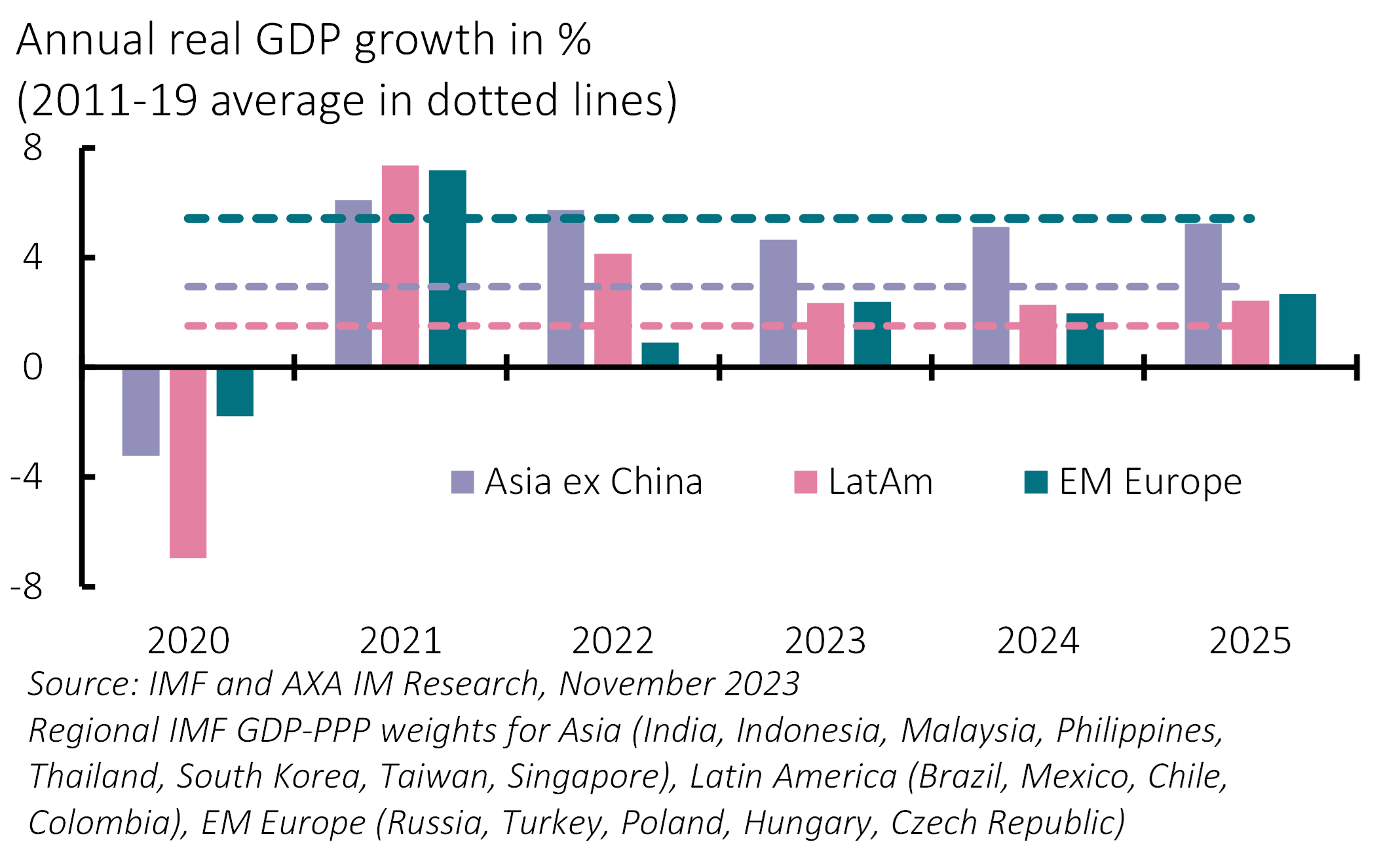

From a bird’s eye view, our 2024 and 2025 EM GDP growth forecasts may appear to suggest quite an impressive resiliency, forecasting overall EM growth of 4.0% in 2024 and 4.1% in 2025, from an expected 3.9% this year – more so as China’s average GDP growth is slowing. Excluding China, growth should pick up from 3.3% to respectively 3.7% and 4.0%. Yet much of this acceleration comes from smaller countries, on which we rely on International Monetary Fund (IMF) estimates, which make up more than 35% of EM ex-China GDP. Our assessment on bigger EM economies is somewhat less rosy as we see growth decelerating in 2024 and stabilising in 2025 along easier monetary policy stances. GDP growth in 2025 is nonetheless expected to remain below its post-financial crisis to pre-pandemic average in both Asia and EM Europe. We see strong divergence between and within regions (Exhibit 1).

Exhibit 1: Nearing post-crisis/pre-COVID-19 growth averages

Asia stands out as the only region forecast to see growth accelerate in 2024. Across Asia, India and Indonesia growth which has held up remarkably well in 2023 is expected to continue, while activity in other smaller economies should also pick up. In Latin America, activity in Brazil and Mexico will decelerate, having been supported by exceptional harvests in the former this year, and with positive spillovers from strong US growth to the latter. Meanwhile, we should see a better backdrop for Chile and Colombia, which have had to deal with issues in the mining sector and political uncertainty this year. EM Europe remains a highly-divided region; Russia and Turkey are expected to slow, while activity in Central Europe should be supported by consumption recovery and European Union funds being partially unlocked in 2024/2025.

Overall, economies will have to cope with weaker, albeit not collapsing, growth in the US. At the same time, positive real rates in the US are likely to continue to exert pressure on the level of nominal rates in EM. Investment may still struggle into early 2024 but external demand could start to benefit from stronger sequential growth in China. Moreover, a recent turnaround in Korean exports suggests the global manufacturing cycle may be slowly turning. We will continue to assess the positive fallouts from adjusting manufacturing supply chains, closer to the developed market consumer (near-shoring in Latin America) and/or away from China (friend-shoring in Asia) via incoming foreign direct investments.

On the consumer side, we could start seeing some benefits of past disinflation improving purchasing power for households. In Central European countries, real wage growth is expected to become positive in 2024. Labour markets have proved resilient so far and we do not envisage a significant deterioration in the years to come. Additionally, according to the IMF, the cumulative excess savings from the COVID-19 period remain across EM, providing a potential cushion to household private consumption, although we may question the uneven distribution of such savings.

Inflation and the Fed to guide monetary easing

Inflation moderated generally more than expected across EMs on the back of supply shocks reabsorption post-pandemic reopening. Energy prices played an important role in the disinflation trend; food price inflation also came off the boil, but risks remain on certain segments on the back of weather-related production disruptions, which could be further distorted by producers imposing export bans, as currently for rice. The possible lifting of remaining price subsidies on fuel or food products in various countries is another upside risk to inflation estimates moving forward. Still, with the notable exception of Turkey, core inflation in EM has come down since its peak roughly a year ago. Headline inflation is expected to reach central banks’ targets at various speeds during the next two years of the forecasting horizon in most countries that we cover. Absent any additional external shock, market focus will move from disinflation to monetary policy easing.

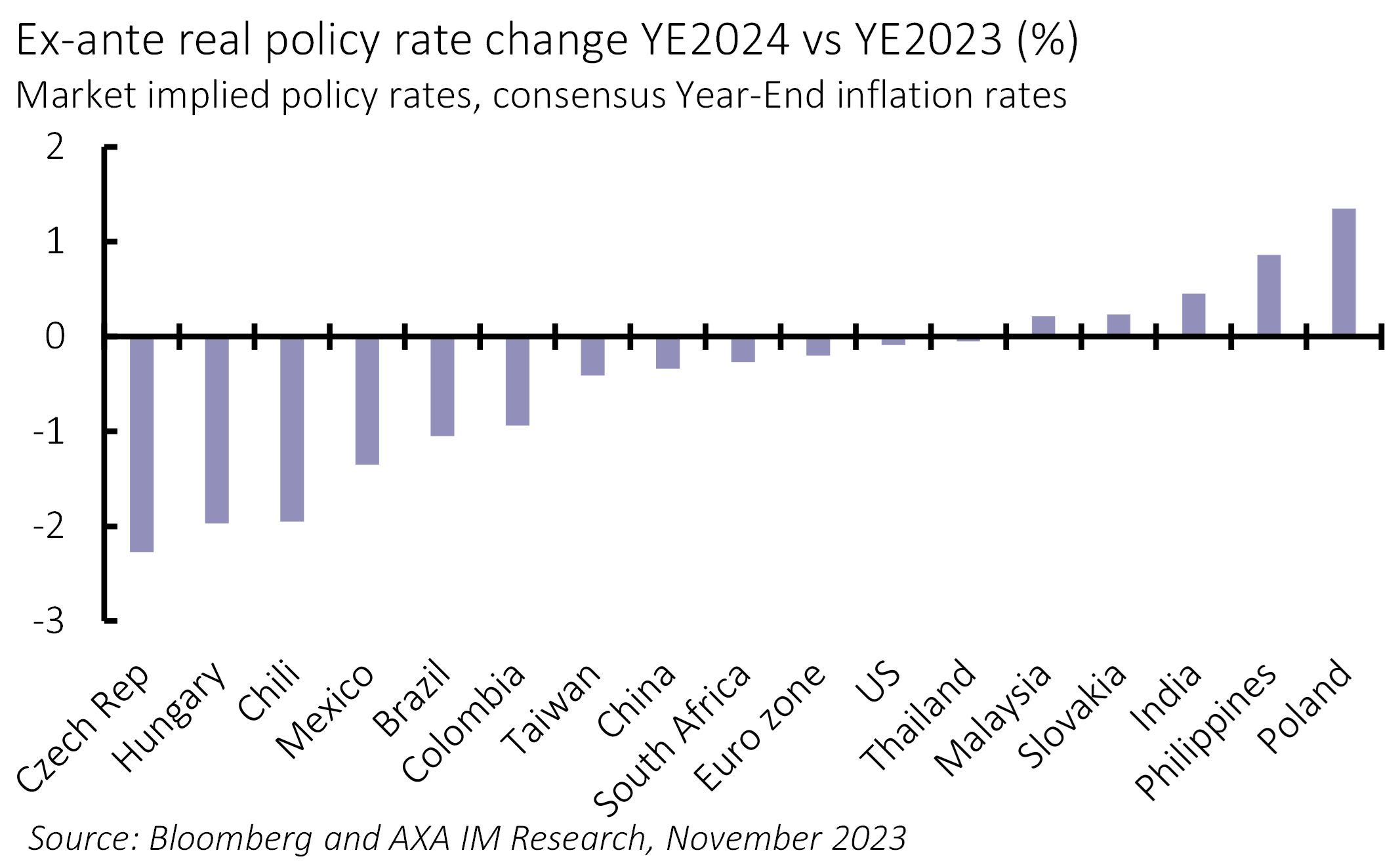

Disinflation allowed several developing countries’ central banks to start cutting policy rates as of 2023, including in Uruguay, Chile, Brazil or Peru across Latin America, Hungary and Poland in EM Europe. More will do so in 2024 and thereafter. Yet we suspect that relatively high US real yields and a strong dollar will prevent aggressive easing, much depending on the pace of disinflation ahead. We note increasing signs of cautiousness among EM central banks that are keen to ensure that inflation is decisively converging on their targets while maintaining the right level of rates to ensure financial stability and maintain foreign investors’ interest. The starkest example being the Bank of Indonesia (BI), which hiked its policy rate by 25bps to 6% in October, having kept rates unchanged since the beginning of the year. Indonesian inflation is close to the lower-end of the BI band (2%-4%) and even though expected to accelerate from here, it should remain well in the BI’s comfort zone. BI rather reacted to the weaker rupiah since April 2023 and reacted preventively to cushion against any souring of foreign investor sentiment. Market-implied ex-ante real policy rates are nonetheless suggesting an easing of the monetary stance in many EM countries in 2024 (Exhibit 2).

Exhibit 2: Monetary policy easing expected ahead

Absent faster-than-expected disinflation and thus against a backdrop of a rather tight monetary stance – outside Asia – governments across EM will feel increasingly constrained as debt loads have risen since 2020 and the increased interest burden is limiting fiscal policy room for manoeuvre. Anti-inflation shields, which supported the consumer this year, should be phased out, and the fiscal impulse is expected to be contractionary but any fiscal consolidation may provide some surprises in the busiest EM electoral year in decades. Tensions between the fiscal and the monetary authorities may become more palpable, and we tend to believe that central banks will respond by more hawkishness (and less dovishness) to fiscal drifts putting downside pressure on our 2025 growth forecasts.

Risks and uncertainties abound, as always

As always, policy gyrations in China and the US, the direction of travel for the US Treasuries, the dollar, geopolitics and commodity prices remain major risks to our EM macro and market outlook. Local politics will come into the spotlight with many elections, be it local, parliamentary or presidential, scheduled in 2024 – starting with Taiwan in January, Indonesia, India and Korea in spring, Mexico and South Africa during summer, Romania and Uruguay towards the year-end, to name a few. Many frontier markets will also come to polls (e.g., Senegal, Ghana, Sri Lanka). The US Presidential Election may nonetheless be the utmost important electoral deadline for EMs this year given its broader and deeper implications as per the possible trade and investment shifts that it could deliver.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.