Changing our Climate: active engagement in oil & gas

We intend to engage with any company that may contribute to a successful transition.

The investee companies

State of Play of their Transition Strategies

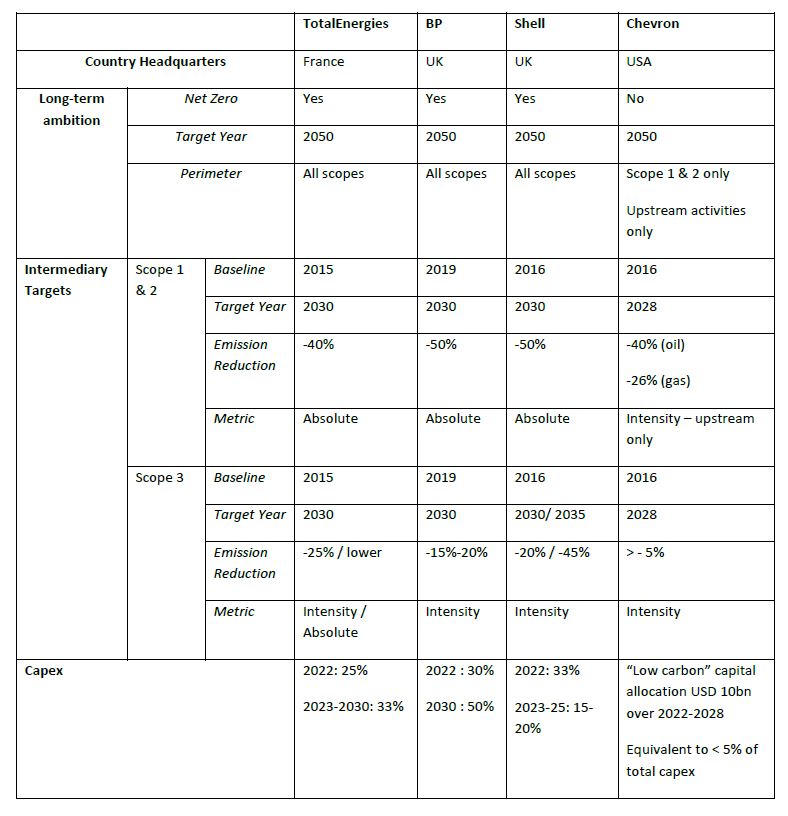

In AXA IM view, in comparison with its peers within the oil and gas sector, TotalEnergies’ strategy appears to be more advanced, and the company is regularly making progress on setting climate-related targets and related-disclosure. Over the past years, the company added new 2025 targets, strengthened its 2030 scope 3 oil target, provided more detailed explanations of how targets will be achieved, and enhanced its scenario analysis and capex disclosure. Earlier this year, the company gave a number for avoided emissions related to LNG sales, highlighting the benefits of natural gas when it displaces a more carbon intensive fuel, most notably coal.

TotalEnergies submitted its transition strategy at its 2021 AGM, which received around 92% support. Since then, it submits annually to shareholder vote a report detailing the progress made against the strategy, which receives stable support from around 89% of votes at the 2022 and 2023 AGMs.

BP presented in September 2020 what we view as a radical corporate reorganisation articulated around its net zero ambitions. The company announced its intention to shrink its upstream division – largely by disposing of assets -, grow its renewable power massively and increase the scale of its client-facing units to sell more low-carbon products. Execution was described as challenging, and the capital required in the early years to be significant (low carbon capex were 3% of total in 2019, 30% in 2022 and the target is 50% in 2030). However, if successful, the strategy will make BP a greener company from 2030 onward. Yet, in February 2023, BP announced a scaling back of its plan to cut O&G output in 2030 from 40% to 25%, due to its decision to sell less assets than initially planned.

BP submitted its transition strategy to a shareholder vote for the first time at its 2022 AGM, which received 88.5% support. The company has not committed to a regular vote on the progresses made (no resolution about this in 2023), although it may submit another vote on its climate strategy in 2025.

Shell’s angle is to leverage on its super-sized marketing footprint – the company sells three times more energy than it produces – and develop low carbon solutions to address the different needs of its customers. LNG – a market where Shell is already the largest player – and petrochemicals will be further developed. Shell has also strong ambitions in carbon sequestration. Shell has set itself a very demanding goal by targeting to be net zero above and beyond its scope 3 perimeter (693Mt), aiming at a much larger self-defined 1,800Mt net carbon footprint. However, we are concerned by the lack of absolute Scope 3 emissions reduction targets and by what we see as an excessive (relative to peers) reliance on nature-based offsets for the company’s 2030 targets. In addition, in June 2023 (hence after the AGM), Shell announced a scale down of its low-carbon investments, from 33% of total investments in 2022 to 15%-20% over 2023-25.

Shell submitted its transition strategy at its 2021 AGM, which received, with 88.7% of support. It has also committed to an annual vote on the progress updates to an annual vote, which recorded in 2022 and 2023 approx. 80% of votes in favour.

Chevron’s energy transition strategy is not as demanding relative to its main European peers. While they have goals to achieve net zero by 2050 for their scope 1, 2 and 3 and across their entire activities, Chevron is limiting this goal to its scope 1 and 2 and to its upstream business, excluding all downstream operations. Chevron is only integrating scope 3 emissions into its targets to reduce emission intensity of its energy sales, and this target is all but demanding. Chevron is more credible when it comes to developing low carbon products such as biofuels, hydrogen and renewable gas, although its peers are pursuing the same avenues. Chevron however, unlike all its European peers, is not planning on developing a renewable electricity business, clearly stressing that it does not want to become an electric utility. Overall, although Chevron has improved its energy transition strategy over the past two years, it is still some way behind the industry leaders in its strategy. Chevron has not yet requested shareholders to vote on its energy transition strategy.

Influencing Change – Our Stewardship Approach

AXA IM regularly engages with TotalEnergies over the years. In 2022, it held four engagement meetings with the company, including one ahead of the 2022 AGM to focus on the vote on the progress report and the Board’s decision to reject the inclusion of a climate-related proposal on the agenda. In 2023 so far, AXA IM held another four meetings, including one focused on the just transition topic. Beyond regular dialogue, AXA IM also used over the years a set of various tools conferred to us as shareholders to gain maximum engagement effect. Firstly, in 2021, AXA IM worked with Climate Action 100+ and signed a statement prepared ahead of the AGM that year. In 2022, multiple discussions were held with other investors and stakeholders to call for a legal clarification on shareholder proposals in France. In 2023, we sent a formal written question to the company ahead of the company’s AGM to publicly state our support for further transparency on avoided emissions from the sale of LNG as well as other energy sources such as sustainable aviation fuels and biomethane.

At the 2023 AGM, AXA IM supported the progress report presented by TotalEnergies, although this will not prevent us to continue engaging and challenging the company privately and publicly to ensure the company progresses in a timely manner in its climate journey. We believe that, when it comes to Scope 3-related reduction targets, a collective effort (including from governments) is needed to ensure an orderly transition. In that respect, TotalEnergies is developing product offerings and technologies that will contribute to changing demand patterns - which, in our view, is the most critical element of the energy transition. This led us to oppose the Scope 3-related resolution submitted by a group of shareholders, although we still discussed at length with the company the Board’s response and communication around Scope 3, as we do not want to see the company shying away from its responsibilities. This will remain a key focus of our engagement with them in the future.

AXA IM held five climate-related engagements in 2022 and 2023 with BP, including one with the Head of Sustainability following their Scope 3-related announcement last February. As the company’s initial Scope 3 targets were mostly linked to selling assets, the decision to keep some of them led to a reduced ambition in the 2030 Scope 3-related objective. In any case, the sale of assets would in essence not contribute to a decrease in the world’s emissions, and the high-level strategy remains fundamentally unchanged (BP is not changing its Scope 1&2 targets for 2030, despite the higher O&G production). As a result, we decided to support BP’s climate strategy in our 2022 vote, and oppose Scope 3-related proposals submitted by shareholders in 2022 and 2023.

Our concerns with BP are related to the communication around the revision in its Scope 3 objectives. What we view as a poorly communicated revision in an otherwise “pragmatic” strategy, reflecting the challenges and contradictions of the transition, comes a few months after the decision from the Board to ask for shareholders’ formal opinion on its strategy and underlying Scope 3 targets. Without providing another opportunity for shareholders to vote on BP’s climate strategy, the conception of “Say on Climate” is rendered less relevant. In that context, we decided to oppose the re-election of the Board Chair at the company’s 2023 AGM.

We met five times with Shell over 2022 and 2023 to discuss climate-related issues, including one following the publication of the 2022 Energy Transition Progress report.

Our main concerns relate to lack of absolute Scope 3 emissions reduction targets as well as a high reliance (relative to peers) on carbon offsets. Hence, we decided to oppose the company’s progress report submitted at the 2023 AGM. This follows two years of support on management sponsored climate-related proposals, illustrating the fact that we aim to accompany investee companies in their transition while not shying away from opposing plans in case absence of meaningful progress is observed over the years. Yet, as we are mindful of the fact that an absolute reduction in the company’s Scope 3 requires a collective effort, we did not support the binding shareholder proposal requesting Paris-aligned absolute Scope 3 targets.

As detailed further above, in AXA IM’s view Chevron’s climate strategy lacks ambition compared to its other European peers. Hence, we have been using over the years the tools at our disposal, including our voting rights, to signal our concerns. At the 2021 AGM, we supported a shareholder proposal asking the company to reduce its Scope 3 emissions which was adopted. Although this led the company to set Portfolio Carbon Intensity targets, these in our view lack ambition as the company continues to consider that the reduction of scope 3 emissions would clash with its business. Chevron is making some investments in low-carbon technologies, but it is unlikely that its plans will lead to an absolute reduction in GHG emissions that is consistent with a “substantial reduction in scope 3 emissions” and thus a limitation of warming to well below 2°C. Given this, at the 2022 AGM, we opposed the re-election of the directors of the public policy and sustainability committee. At the 2023 AGM, we decided to further escalate and collaborated with other investors and NGO Follow This to co-file a Scope 3-related resolution at the agenda of the 2023 AGM.

Disclaimer

Companies shown are for illustrative purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.